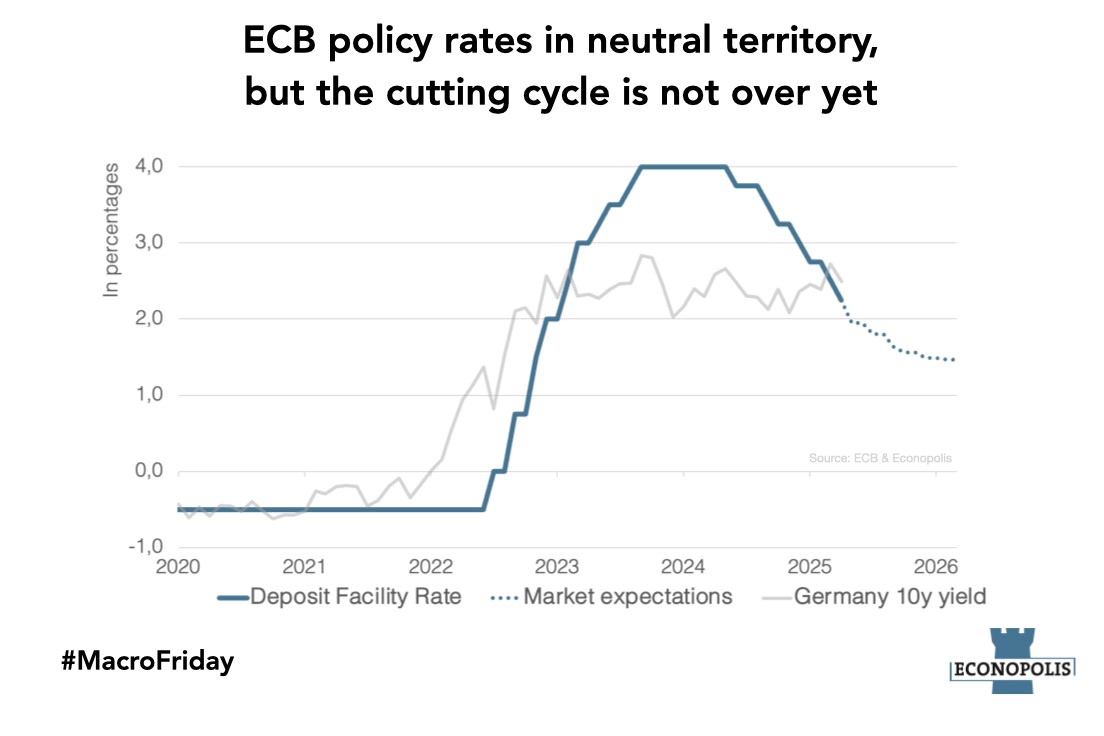

#MacroFriday: ECB Policy Rates in Neutral Territory, but the Cutting Cycle is Not Over Yet

This week, the ECB announced its seventh rate cut in the past year. With the deposit facility rate now at 2.25%, we are back in what could be considered as ‘neutral’ territory.

However, the ECB avoided describing the ‘level of restrictiveness’ in its policy statement, noting that such a comparison requires an economic framework free of shocks. This comment by President Lagarde immediately highlighted the uncertain economic environment in the eurozone shaped by a negative demand shock, something she frequently acknowledged during the press conference. Lagarde also noted that the Governing Council would likely have opted for a pause in rate cuts just a few weeks ago. But the outlook has become increasingly uncertain.

Why did the ECB cut rates then?

While the expected impact of tariffs on economic growth in the eurozone is negative due the negative demand shock, the effect on inflation remains unclear. The recent strengthening of the euro, both against the USD and in trade-weighted terms, combined with falling oil prices, have disinflationary effects. Over the medium term, the ECB is less certain about the inflaton path. On one hand, global protectionist measures and deglobalisation could push prices higher; on the other, export rerouting from countries with overcapacity and weaker economic growth could dampen inflationnary pressures.

Meanwhile, services inflation in the euro has finally been trending down since the beginning of the year.

Given persistent uncertainty in the global economy and ongoing trade tensions, the ECB is likely to continue cutting its key policy rates. Markets are currently pricing in three additional rate cuts in 2025, with the next one expected at June meeting.

comments powered by Disqus