#MacroFriday: European Services Inflation holds firm

We kick off this new MacroFriday year in Europe with the publication of December’s inflation numbers this week. And, the inflation struggle is far from over.

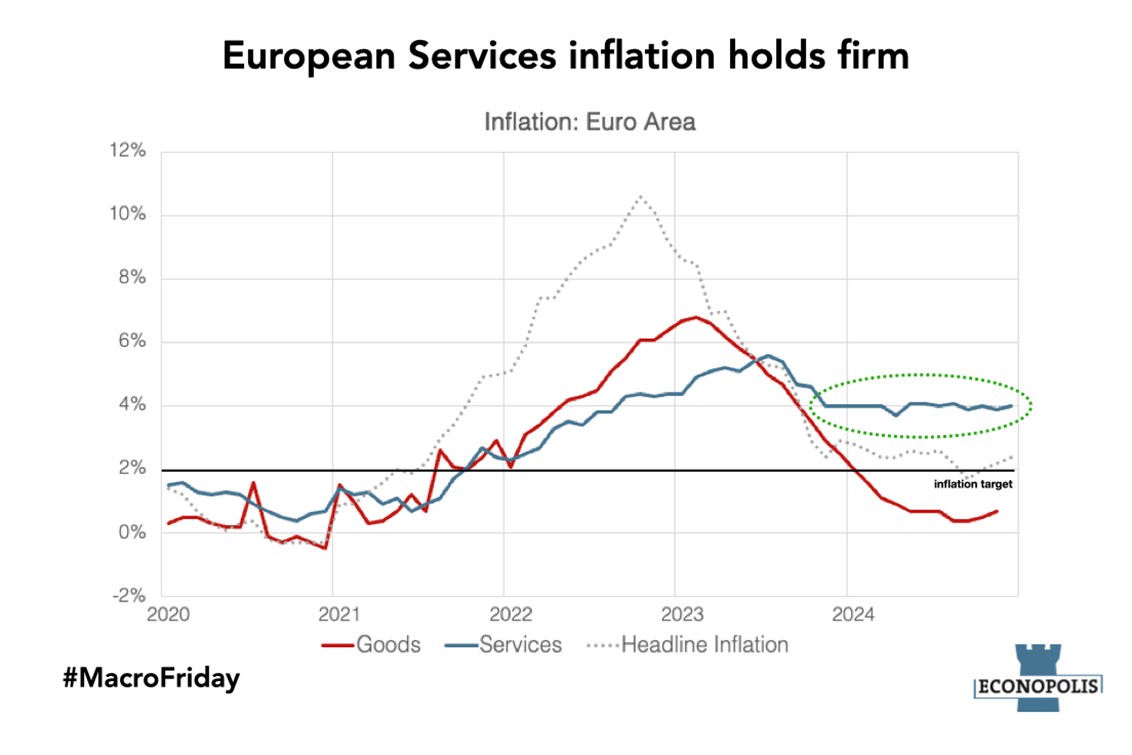

Headline inflation in the Euro Area dropped to 1.8% in September, falling below the ECB’s inflation target of 2%. At that time, inflation had reached its lowest level since June 2021. Since then, inflation has picked up again, driven primarily by rising food prices (2.7%) and a slight increase in energy prices (0.1%). Natural gas prices remain well above last year’s levels, and oil prices are no longer declining. Meanwhile, services inflation has remained steady at 4% for more than a year. Given its 44.88% weighting in the inflation basket, the ECB needs services inflation to ease in order to sustain the disinflationary trend and continue its rate-cutting cycle.

Unfortunately for the ECB, wage growth has a significant impact on services inflation and has remained elevated in recent quarters. Labor market conditions in the Euro Area are still tight, with the unemployment rate standing at a record low of 6.3%. In November, unemployment decreased by 39,000. While the stagnating European economy calls for lower interest rates, the inflation battle is far from won. It seems the ECB governors are currently more concerned about economic growth prospects in the Euro Area than about the recent uptick in inflation. For investors, activating savings and staying invested remain crucial strategies to mitigate the potential loss of purchasing power.

I conclude by wishing you all the best for the new year.

May the markets be in your favor!

comments powered by Disqus